I used to think earnings beats moved stocks up. Simple as that. Company does better than expected, shares rise. That’s the deal.

Then I watched Tesla deliver one of the best quarterly numbers in its history on July 2, 2026 — and get punished for it. Shares sank roughly 7.5%, the worst single-day drop the stock has seen in nearly a year. Not because Tesla missed. Because it beat, and beat big, and Wall Street decided that wasn’t the point anymore.

If you’re trying to make sense of that, you’re not alone. Here’s what actually happened, and why “good news” and “stock goes up” stopped being the same sentence.

The Numbers Were Genuinely Great

Let’s start with what Tesla actually delivered, because the numbers deserve credit before we get into why nobody rewarded them.

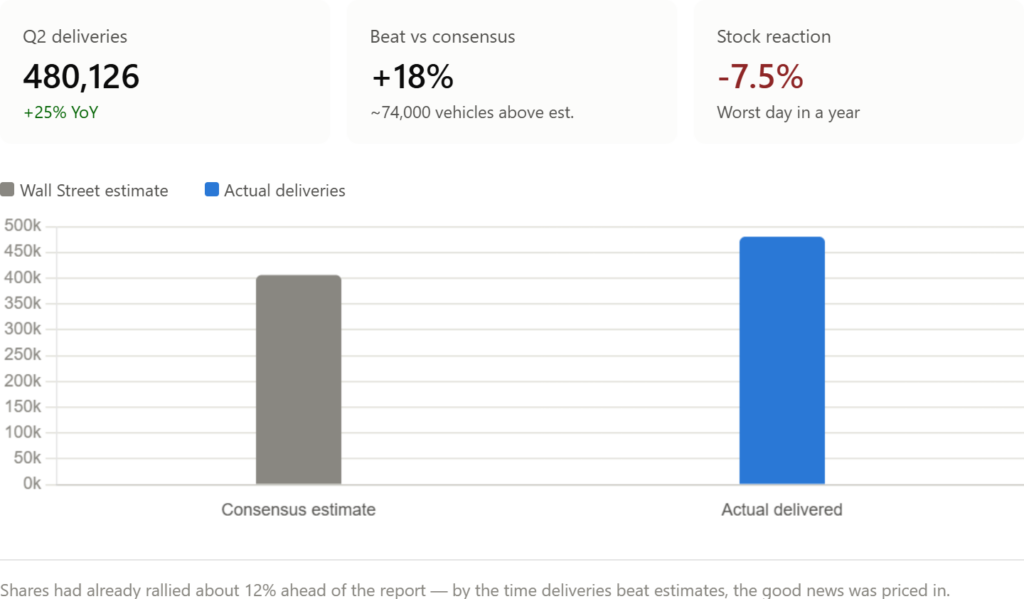

Tesla shipped 480,126 vehicles in the second quarter of 2026, a 25% jump from the same period last year. That also marked a 34% increase over the first quarter’s 358,023 deliveries. For a company that had just come off two straight years of annual sales declines, that’s not a modest recovery. That’s a company slamming the brakes on a downward trend.

Wall Street wasn’t ready for it, either. The company-compiled consensus estimate sat around 406,000 vehicles. Tesla beat that by roughly 74,000 units — close to 18% above expectations. One independent delivery analyst, Troy Teslike, had actually come closer than most of Wall Street with a forecast of 466,000, and he still undercalled the real number.

Morgan Stanley’s Andrew Percoco called it the strongest auto growth Tesla had posted since late 2023. Deepwater Asset Management’s Gene Munster went further, describing it as a “monster” quarter that likely marks the end of the EV slump that had been dragging on since early 2024.

By almost every traditional measure, this was a quarter worth celebrating.

So Why Did the Stock Fall?

Here’s the part that trips people up: the stock didn’t fall because of the delivery report. It fell because of what happened before the delivery report.

In the weeks leading up to July 2, Tesla shares had already climbed roughly 12%. Traders were positioning themselves for exactly the kind of blowout quarter Tesla ended up posting. Some of that run-up traced back to June 29, when Tesla shares jumped more than 8% in a single day on excitement around the FSD v14 Lite software rollout, which finally reached older Hardware 3 vehicles for the first time in over a year.

By the time the actual delivery numbers landed on Thursday, the good news was already priced in. Traders who’d bought ahead of the report did what traders do after a run-up: they took profits. Shares actually ticked up about 2% in early trading before sliding into the red as the session went on.

This is a pattern investors call “sell the news,” and it’s not new. It happens when expectations run so far ahead of reality that even a genuinely strong result can’t clear the bar the market quietly set for itself.

The Bigger Problem: Deliveries Aren’t the Story Anymore

There’s a deeper shift happening here, and it’s worth sitting with.

Tesla’s roughly $1.6 trillion valuation isn’t really built on car sales anymore. It’s built on the promise of robotaxis, Full Self-Driving, and Optimus, the humanoid robot Musk has positioned as the company’s next act. When Tesla trades like an AI and robotics company rather than an automaker, a strong quarter of car deliveries — even a record one — doesn’t move the needle the way it used to.

One retail investor summed up the mood well in a Stocktwits thread following the sell-off: investors aren’t satisfied with strong car numbers alone anymore. The valuation now leans on FSD, robotaxis, and Optimus delivering results, not just Model 3s and Model Ys rolling off the lot.

Truist analyst William Stein raised his price target on the stock following the report, but flagged something telling in his note: there was no fresh update on AI initiatives or new vehicle programs. For a stock priced on future technology, silence on that front matters more than a delivery beat.

There’s also a manufacturing wrinkle worth mentioning. Tesla delivered more vehicles than it produced this quarter — 480,126 delivered against 451,758 produced. That’s good for clearing out inventory in the short term, but it’s not something a company can do indefinitely. At some point, production has to catch up, and that shifts the conversation toward capital spending and manufacturing efficiency rather than pure demand.

What Actually Drove the Demand

It’s also worth being honest about where some of this growth came from, because it complicates the “Tesla is back” narrative a little.

Cox Automotive’s Stephanie Valdez-Streaty pointed to rising gas prices, tied to the conflict involving Iran, as a meaningful tailwind — particularly in Europe, where EV sales have been climbing in recent months. Tesla’s cheaper Model 3 and Model Y variants, introduced to reignite demand after a rough stretch, also played a role. Together, Model 3 and Model Y accounted for 97% of everything Tesla delivered in the quarter.

That doesn’t take anything away from the number itself. But it does explain why some analysts, including fund manager Gary Black, are treating the beat with a bit of caution rather than pure celebration — the concern being how much of this growth is durable demand versus a temporary boost from gas prices and pulled-forward sales.

What Happens Next

Tesla reports full second-quarter financial results on July 22. That’s the report that will actually tell the real story — not how many cars Tesla moved, but what it made on each one.

If the delivery beat came with healthy margins and disciplined pricing, expect the market to warm back up to the stock. If it came from heavy incentives and discounting to hit those numbers, the July 2 sell-off might look like the start of a trend rather than a one-day blip.

There’s also an ongoing safety probe from the National Highway Traffic Safety Administration tied to a fatal June crash involving Tesla’s driver-assistance software — a detail that matters given how much of Tesla’s future valuation rests on that same technology stack powering its robotaxi ambitions.

For now, despite Thursday’s drop, Tesla stock was still up about 4% for the week. Zoom out further and it’s down roughly 13% year-to-date. Neither number tells the whole story on its own, which is sort of the point of this entire episode: with Tesla, the headline number rarely is the whole story.

Let’s Cover Some Questions

Why did Tesla stock drop after beating delivery estimates? The stock fell mainly because expectations had already been priced in before the report. Shares rallied roughly 12% in the weeks leading up to the announcement, so by the time the record 480,126 deliveries were confirmed, investors used the news as a reason to lock in gains — a classic “sell the news” reaction.

How many vehicles did Tesla deliver in Q2 2026? Tesla delivered 480,126 vehicles, a 25% increase year-over-year and a 34% jump from the first quarter. That beat Wall Street’s consensus estimate of roughly 406,000 by about 18%.

Is Tesla’s stock decline a sign of trouble? Not necessarily. Many analysts, including those at Morgan Stanley and William Blair, maintained or raised their price targets after the report. The drop reflects short-term profit-taking and shifting investor focus toward AI, robotaxis, and margins rather than a loss of confidence in the delivery numbers themselves.

When will Tesla report full Q2 earnings? Tesla is scheduled to release its complete second-quarter financial results on July 22, 2026, which will include revenue, margins, and forward guidance.

What’s driving investor focus away from car deliveries? Tesla’s valuation increasingly rests on Full Self-Driving, robotaxi expansion, and the Optimus humanoid robot program. Analysts note that strong car sales alone no longer satisfy a market pricing Tesla like an AI and robotics company rather than a traditional automaker.